Subscribe to Our Newsletter

Read the latest in the world of AI, data center, and edge innovation.

On June 16, a rocket company bought a coding assistant for $60 billion.

Four days off the largest IPO in financial history, SpaceX agreed to acquire Anysphere, the startup behind the AI coding tool Cursor, in an all-stock deal. It was the biggest purchase of a venture-backed company on record. The buyer builds reusable rockets and beams internet from low orbit. The target builds software that writes code. On paper, the two have nothing to do with each other, and that is the whole point.

In March, we published an article highlighting the shift from a race for the smartest model to a scramble for the power, pipes, and provenance that make a model useful. The last 90 days of acquisitions moved the storyline again. The layers are no longer holding as separate tiers. The action shifted to the layers above the model, and orchestration became the hottest prize of all. A handful of owners are now reaching to control every tier at once. And vertical integration stopped being a strategy. It became the entire game.

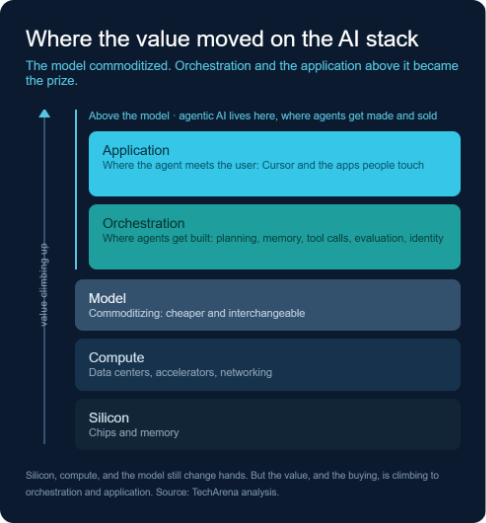

Picture the AI stack as five tiers. For three years, the model at its center was the product and the prize. That has flipped. Models keep getting cheaper and more interchangeable, and the value is climbing to the two tiers above them. Orchestration is where an agent gets built: planning, memory, tool calls, evaluation, the identity it uses to log in. The application layer is where that agent meets a user, the way Cursor meets a developer. Agentic AI lives in those upper tiers, software that plans and acts instead of only answering. The buying is a race to own that ground.

Global M&A cleared $1.2 trillion in the first quarter of 2026. The number of deals fell from a year earlier, but the ones that closed were bigger. Twenty-two transactions topped $10 billion, a quarterly record. AI drove four of the six largest.

The shape of the money is as telling as the size. Equity-stake purchases, not clean acquisitions, made up 29% of deal volume. OpenAI’s raise, which closed at $122 billion, counted as three of the quarter’s biggest transactions on its own. Anthropic’s $30 billion round tied for fourth. The line between buying a company and funding one has gone soft, and that blur runs through everything below.

Pull the megadeals aside and look at what actually changed hands this spring, and almost nobody bought a model. They bought agents, the applications people actually use, and the orchestration machinery that makes those agents work.

Cursor is an agent that writes code. Manus, the autonomous agent Meta agreed to buy earlier in the year for $2 billion before regulators stepped in, runs multi-step jobs on its own. Around those headline targets, a quieter shopping spree filled in the plumbing. Anthropic paid a reported figure of more than $300 million for Stainless, the tooling startup whose SDKs and MCP servers are used by OpenAI, Google, and Cloudflare. Databricks bought Quotient AI to grade agents on their own production traces. DigitalOcean took Katanemo Labs to run agentic inference. ServiceNow moved on Veza to handle identity when the thing logging in is a machine, not a person. OpenAI absorbed Astral, the team behind the open-source Python tools half the AI world already builds on, and bought Ona, the cloud-execution startup once known as Gitpod, so its Codex agents can run for hours inside a customer’s own cloud. SAP closed its purchase of Dremio in early July to turn its data platform into an agent-ready lakehouse. The consolidation reached the orchestrators themselves. On July 13, Prefect agreed to buy Dagster Labs, folding the two most widely adopted successors to Apache Airflow into one workflow engine that runs data pipelines and agentic jobs and governs agents through the Model Context Protocol.

Line them up and a category snaps into focus. Coding, autonomy, evaluation, inference, identity, tooling, workflow. None of it is a foundation model. All of it is the orchestration layer, the tier that turns a model into something that works and can be trusted to run without a human watching every keystroke. Read another way, it is a list of the bottlenecks between a clever demo and a production system, each one bought by the company that felt the pinch first.

“Everyone has been focused on who is winning the AI model race. The bigger question is who controls the production stack,” said Laura St. John, TechArena co-founder and advisor. “We’re seeing companies acquire the technologies that turn AI from pilots into production-ready platforms, capturing the layers that make AI deployable, manageable, and repeatable in the enterprise. Cloud followed a similar path: proprietary ecosystems dominated early, then enterprises pushed for portability and choice. The question is whether AI follows the same trajectory once buyers begin to feel the tradeoff between capability and lock-in.”

The other force is the one SpaceX put in neon. Buying Cursor is not a coding play. It is the capstone on a structure that already runs from the power source to the orbit to the social feed. Reusable launch. Starlink satellites. The xAI merger that folded in models and the X platform. Now the application layer, the agent that sits in front of a developer all day.

Qualcomm reached the other way. At its June 24 Investor Day, the smartphone chip company confirmed a $3.92 billion all-stock deal for Modular, the software startup founded by Chris Lattner, the engineer behind LLVM and Apple’s Swift. Modular’s platform lets AI models run across CPUs, GPUs, NPUs, and custom silicon without rewriting code for each one, a direct strike at the CUDA software lock-in that has kept developers tethered to Nvidia. Qualcomm wrapped it into a new Dragonfly data-center chip line, lined up anchor commitments from Meta and Microsoft, and may not be done. The company has reportedly been in talks to buy Tenstorrent, Jim Keller’s RISC-V accelerator startup, for as much as $10 billion, a deal that stayed unconfirmed at the event.

SpaceX bought its way up the stack toward the user. Qualcomm bought its way across it, from silicon into the software that decides which silicon a developer can use. Different directions, one instinct: own the layer you are missing.

The frontier labs are running the same move in a lower key. OpenAI stood up a Deployment Company, a $4 billion services venture, and bought a consulting firm to staff it with forward-deployed engineers. Anthropic helped stand up a new Blackstone-backed enterprise-services firm, reinforcing the tooling layer with Stainless, and pushed into biology with a roughly $400 million deal for the drug-discovery startup Coefficient Bio.

In July, Microsoft matched the pattern from its own perch, committing $2.5 billion and 6,000 people to a dedicated AI deployment unit. These are not the moves of companies that see themselves as model vendors. They are the moves of companies building everything above and below the model, then selling the whole stack as one thing.

Lynn Comp, vice president and head of global sales and go-to-market for Intel’s AI Center of Excellence and a TechArena Voice of Innovation, reads the pivot as a structural inevitability.

“While the frontier models were largely focused on a race with one another and the pursuit of ‘AGI’, it was clear that any general-purpose model would likely fall into a class of software known as middleware, that historically struggles to maintain stickiness and margin,” she said. “The fact that the frontier labs and their hyperscaler hosts are now investing in services confirms that the model alone will not maintain long term value when it comes to the enterprise buyer.”

The reflex reaches past software. In space, the field SpaceX helped define, Rocket Lab agreed in late June to buy the satellite operator Iridium for $8 billion, stitching launch and network together to compete with Starlink. The move is the same whether the target is an agent or an orbit.

The moat has become the number of layers you control.

As the software layers consolidated, a parallel land grab opened in the physical world. Amazon bought Fauna Robotics, a humanoid startup aimed at everyday spaces rather than warehouses. Meta picked up Assured Robot Intelligence to sharpen the models that run robot bodies. Google folded in Intrinsic, the industrial-robotics software group it had been incubating. SoftBank folded Green Clean Commercial into a new Smart Building X unit.

The logic is the one driving the software deals, pointed at hardware. If the goal is owning the full stack, the stack does not stop at the screen. It runs into the arm, the gripper, the chassis. AI has lived on a screen. Its next form factor has arms, and those companies are changing hands now.

When a single funding round outweighs most of the quarter’s acquisitions, the league tables stop measuring what they used to.

The circularity is hard to miss once you see it. Nvidia invested $2 billion in Marvell, one of its own suppliers, in March. Apollo and Blackstone led a reported $35 billion financing platform, announced June 9, tied to Broadcom’s AI infrastructure and the compute buildouts of labs including Anthropic and OpenAI. Chips, capital, and compute now flow in loops between the same dozen companies. A supplier funds a customer who buys from a partner who invests back in the supplier.

The buying runs all the way to the sensor. ON Semiconductor struck a $7 billion deal for Synaptics on June 25 to push into physical AI, the chips that let machines see, touch, and read a room. When the prize is the whole stack, the silicon that feeds the robot counts as much as the model that steers it.

Comp offers a way to read where the buying lands next.

“In database and data platforms there is an operational triad called ‘ETL’ (Extract, transform, load). For hardware infrastructure, there is an equivalent that holds true at every layer of the tech stack from inside the compute pipeline to the SOC up to the datacenter itself: First: Network/Bandwidth. Second: storage/memory and lastly: processing/compute. The hardware industry is always trying to achieve balance between the three and always over-building in one domain, only to discover the bottleneck moves to one of the other two,” she said.

The squeeze is moving to memory. AMD bought MEXT on June 15, a Santa Clara startup whose software makes flash behave like DRAM and stretches usable memory without buying more of it. The timing is not incidental. DRAM supply is growing slower than demand, and Gartner expects combined DRAM and SSD prices to climb roughly 130% by the end of 2026. When memory gets scarce, the companies building AI infrastructure stop waiting for the market to loosen and start buying the engineers who can wring more out of what they already have.

Memory gave the clearest read of all. On June 24, Micron, the only U.S. maker of the high-bandwidth memory that feeds every major AI accelerator, posted record fiscal third-quarter revenue of $41.5 billion, gross margin of 84.9%, and earnings of $25.11 a share, past every Wall Street estimate. It guided the next quarter to roughly $50 billion, said it is sold out of HBM into 2027, and watched its stock jump about 15%. The largest hyperscalers have committed more than $725 billion to AI infrastructure this year, and the industry watches Micron to learn whether that spending is holding. The answer was not subtle. Memory is where the buildout shows up first, and the meter is still climbing.

Governments are the one force pushing the other way, and they cut from two directions. The clearest is the agent deal that did not close. Beijing blocked Meta’s $2 billion purchase of Manus and ordered the company to unwind it, treating the startup’s China-developed technology as an export to control rather than an asset to sell. The other direction is antitrust. When Nvidia took Groq’s inference technology and talent late last year in a licensing-plus-hiring arrangement rather than a clean buyout, Sens. Elizabeth Warren and Richard Blumenthal sent a letter asking whether the structure was an end run around review. Expect more of both questions. The deals are getting creative precisely as the scrutiny gets sharper.

All of that dealmaking points to a question not answered in the last few months. Cloud computing became a utility the day it stopped mattering which cloud you used, once a portable unit of work and a neutral steward, the Cloud Native Computing Foundation, let enterprises move between providers at will. AI has the compute and the model APIs. It does not yet have a portable layer or a neutral body to govern one. The candidates keep getting bought before they can open, from agent tooling to the run-anywhere software Qualcomm just folded into its own silicon.

A few buyers are moving the other way. On July 10, Scaleway, the sovereign European cloud arm of the iliad Group, bought the French HPC specialist Qarnot and built the deal on open standards rather than around them. Both companies design their infrastructure to Open Compute Project specifications, and both pitch portability and freedom from lock-in as the product itself. Qarnot brings patented liquid cooling that recovers up to 95% of the heat its servers throw off and pipes it into district heating networks, already running in cities such as Brescia, Italy. Set against the megadeals, it is a small transaction. It also points straight at the layer the open camp still hopes to build, and it does so from Europe, where sovereignty gives portability a second reason to exist.

History says an open wave still comes. It came for cloud after years of walled gardens like AWS, and the fragmented open efforts in AI are moving faster than cloud’s early ones did. The push has not hit its tipping point, the moment that shoves it to the front. When it does, expect it to run through the groups built for exactly this fight, the Open Source Initiative and the Linux Foundation. That is the open question underneath all the buying.

For startups, the gap only widened. In our March AI M&A article, I called it the integration gap, the distance between owning one clever capability and owning enough of the stack around it to deliver that capability and govern it in production. A year ago, that gap was a step. Now it is a canyon.

If your product is one sharp capability without the layers around it, you are not a platform. You are a feature, and features get bought or buried. The companies that sold in the first and second quarters of 2026 were a missing floor in someone else’s building. The ones that did not sell are racing to add floors of their own before the offer comes.

For enterprises, the vendor you pick now arrives with a stack bolted on. Lock-in used to mean a model or a database. It is starting to mean everything underneath, from the agent down to the silicon. That is convenient right up until it is not. The demand worth making now, loudly, is for portability. No vendor will offer it unprompted.

For the industry, the contest is no longer about owning a layer. It is about how few players end up owning the whole run, from the power plant to the prompt. Whether AI ends up a utility or a set of fiefdoms turns on whether a neutral, portable layer survives the buying. That is the story to watch, and the one we report next.

-----

1. Reuters, “Global first-quarter M&A exceeds $1.2 trillion, led by AI,” April 1, 2026. https://www.reuters.com/business/finance/global-first-quarter-ma-exceeds-12-trillion-led-by-ai-2026-04-01/

2. CNBC, “SpaceX to acquire the AI coding startup Cursor for $60 billion,” June 16, 2026; corroborated by TechCrunch, June 16, 2026. https://www.cnbc.com/2026/06/16/spacex-spcx-cursor-acquisition-ipo.html

3. Rachel Horton, “2026 AI M&A: The Great Shift from Models to Infrastructure,” TechArena, March 10, 2026. https://techarena.ai/content/2026-ai-m-a-the-great-shift-from-models-to-infrastructure

4. TechRadar, “Meta buys Manus for $2 billion to power high-stakes AI agent race,” 2026 (announced deal). https://www.techradar.com/pro/meta-buys-manus-for-usd2-billion-to-power-high-stakes-ai-agent-race

5. CNBC, “China blocks Meta's acquisition of AI startup Manus,” April 27, 2026 (China's NDRC ordered Meta to unwind the deal). https://www.cnbc.com/2026/04/27/meta-manus-china-blocks-acquisition-ai-startup.html

6. TechCrunch, “Anthropic has acquired the dev tools startup used by OpenAI, Google, and Cloudflare” (Stainless), May 18, 2026. https://techcrunch.com/2026/05/18/anthropic-has-acquired-the-dev-tools-startup-used-by-openai-google-and-cloudflare/

7. PrivSource, “Databricks Acquires Quotient AI to Power AI Agent Evaluations,” March 19, 2026. https://www.privsource.com/acquisitions/deal/databricks-acquires-quotient-ai-to-power-ai-agent-evaluations-4dS397

8. PrivSource, “DigitalOcean Acquires Katanemo Labs to Expand Agentic AI Inference Cloud,” April 2, 2026. https://www.privsource.com/acquisitions/deal/digitalocean-acquires-katanemo-labs-to-expand-agentic-ai-inference-cloud-VnSWDA

9. ServiceNow Newsroom, “ServiceNow to Expand Security Portfolio With Acquisition of Veza's Leading AI-native Identity Security Platform,” 2025; deal closed March 2, 2026. https://newsroom.servicenow.com/press-releases/details/2025/ServiceNow-to-Expand-Security-Portfolio-With-Acquisition-of-Vezas-Leading-AI-native-Identity-Security-Platform/default.aspx

10. Crunchbase News, “Data: OpenAI Has Already Done Nearly As Many M&A Deals In 2026 As It Did All of Last Year” (Astral), 2026. https://news.crunchbase.com/ma/data-openai-2023-2026-acquisitions-open-source-astral-promptfoo/

11. SAP News Center, “SAP Completes Dremio Acquisition,” July 2026. https://news.sap.com/2026/07/sap-completes-dremio-acquisition/

12. The Guardian, “Elon Musk is taking SpaceX's minority shareholders for a ride,” February 3, 2026. https://www.theguardian.com/business/nils-pratley-on-finance/2026/feb/03/elon-musk-is-taking-spacexs-minority-shareholders-for-a-ride

13. Network World, “Qualcomm's $3.9 billion purchase of Modular aims to change the data center dynamic,” June 24, 2026; see also Quartz, June 24, 2026. https://www.networkworld.com/article/4189098/qualcomms-3-9-billion-purchase-of-modular-aims-to-change-the-data-center-dynamic.html

14. TechTimes, “Qualcomm Bets $14 Billion on Cracking Nvidia's AI Monopoly With RISC-V and an Open Compiler,” June 24, 2026; Qualcomm Investor Relations, Investor Day 2026. https://www.techtimes.com/articles/319017/20260624/qualcomm-bets-14-billion-cracking-nvidias-ai-monopoly-risc-v-open-compiler.htm

15. The Information, “Qualcomm in Talks to Buy Tenstorrent to Expand AI Chip Capabilities,” June 15, 2026; see also TechTimes, June 17, 2026. https://www.theinformation.com/articles/qualcomm-talks-buy-tenstorrent-expand-ai-chip-capabilities

16. OpenAI, “OpenAI launches the OpenAI Deployment Company to help businesses build around intelligence,” 2026. https://openai.com/index/openai-launches-the-deployment-company/

17. Bloomberg, “Anthropic-Backed AI Services Firm Acquires Fractional AI in First Deal,” May 21, 2026. https://www.bloomberg.com/news/articles/2026-05-21/anthropic-s-new-consulting-venture-makes-its-first-acquisition

18. FierceBiotech, “Anthropic acquires stealth AI startup Coefficient Bio in $400M deal: reports,” 2026. https://www.fiercebiotech.com/biotech/anthropic-acquires-stealth-ai-startup-coefficient-bio-400m-deal

19. TechCrunch, “Microsoft launches its own AI deployment company with $2.5 billion commitment,” July 2, 2026; see also CNBC, July 2, 2026. https://techcrunch.com/2026/07/02/microsoft-launches-its-own-ai-deployment-company-with-2-5-billion-commitment/

20. The Motley Fool, “Rocket Lab Announces a Big Acquisition That Could Be Problematic for SpaceX” (Iridium, $8 billion), July 7, 2026. https://www.fool.com/investing/2026/07/07/rocket-lab-announces-a-big-acquisition-that-could/

21. PrivSource, “Amazon Acquires Fauna Robotics,” March 27, 2026. https://www.privsource.com/acquisitions/deal/amazon-acquires-fauna-robotics-deSlo5

22. TechCrunch, “Meta buys robotics startup to bolster its humanoid AI ambitions,” May 1, 2026. https://techcrunch.com/2026/05/01/meta-buys-robotics-startup-to-bolster-its-humanoid-ai-ambitions/

23. PrivSource, “Google Absorbs Intrinsic to Build Physical AI for Industrial Robotics,” March 1, 2026. https://www.privsource.com/acquisitions/deal/google-absorbs-intrinsic-to-build-physical-ai-for-industrial-robotics-4dSW72

24. PrivSource, “SoftBank Robotics America Acquires Green Clean Commercial to Launch Smart Building X (SBX),” March 24, 2026. https://www.privsource.com/acquisitions/deal/softbank-robotics-america-acquires-green-clean-commercial-to-launch-smart-building-x-sbx-2VSmwj

25. Crunchbase News, “Sector Snapshot: Semiconductor Startup Funding Still Running Hot,” 2026 (Nvidia's $2 billion strategic investment in Marvell, NVLink Fusion). https://news.crunchbase.com/semiconductors-and-5g/chip-startup-funding-2026-cerebras-matx-ayar-labs-ipos-nvda/

26. PR Newswire, “Broadcom, Apollo, and Blackstone Establish Landmark Strategic Platform to Accelerate More Than 20 Gigawatts of Global AI Deployments,” June 2026. https://www.prnewswire.com/news-releases/broadcom-apollo-and-blackstone-establish-landmark-strategic-platform-to-accelerate-more-than-20-gigawatts-of-global-ai-deployments-302795286.html

27. CNBC, “ON Semiconductor strikes $7 billion deal for Synaptics in physical AI push,” June 25, 2026. https://www.cnbc.com/2026/06/25/on-semi-synaptics-deal-physical-ai.html

28. AMD, “AMD Acquires MEXT to Advance Memory Optimization for Compute Infrastructure,” June 15, 2026; see also SiliconANGLE, June 15, 2026. https://www.amd.com/en/blogs/2026/amd-acquires-mext-for-memory-optimization.html

29. Tom's Hardware, “AMD takes over MEXT for memory tiering tech,” June 2026; Gartner DRAM/SSD price forecast cited in Network World, June 2026. https://www.networkworld.com/article/4186201/amd-acquires-mext-to-add-predictive-memory-optimization-to-its-ai-stack.html

30. CNBC, “Micron (MU) earnings report Q3 2026,” June 24, 2026; StockTitan, June 24, 2026. https://www.cnbc.com/2026/06/24/micron-mu-earnings-report-q3-2026.html

31. StockTitan, “Micron posts $41.5B Q3 revenue, guides Q4 to $50B,” June 24, 2026; Investing.com earnings call transcript, June 24, 2026. https://www.stocktitan.net/news/MU/micron-technology-inc-reports-record-results-for-the-third-quarter-6f50161e5zxh.html

32. IntuitionLabs, “Nvidia's $20B Groq Acquisition: Why It Paid 2.9x Valuation for LPU Tech,” 2026 (details the March 2026 Warren-Blumenthal antitrust letter). https://intuitionlabs.ai/articles/nvidia-groq-ai-inference-deal

33. Laura St. John, TechArena co-founder and advisor, from feedback shared with the author, July 2026. Quote is a proposed distillation pending her approval.

34. HPCwire, “Scaleway Acquires Qarnot to Add HPC Capabilities to European Cloud Platform,” July 10, 2026. https://www.hpcwire.com/off-the-wire/scaleway-acquires-qarnot-to-add-hpc-capabilities-to-european-cloud-platform/

35. Yahoo Finance / Business Wire, “Prefect Acquires Dagster, Uniting the Two Leading Modern Orchestrators,” July 13, 2026. https://finance.yahoo.com/technology/ai/articles/prefect-acquires-dagster-uniting-two-120000451.html

36. OpenAI, “OpenAI to acquire Ona,” June 11, 2026; see also CNBC, June 11, 2026. https://openai.com/index/openai-to-acquire-ona/